Not all savings accounts work the same way. Some are designed for everyday savings and emergency funds, while others are better suited for larger balances or long-term financial goals.

Understanding the different types of savings accounts can make it easier to choose the right option for your needs. The best account depends on what you're saving for, when you’ll need access to your money, and how you want your savings to work for you.

In this guide, we’ll walk through several savings account options so you can compare features, understand how each account works, and choose an option that fits your goals.

Understanding Savings Account Types

Before choosing a savings account, it helps to understand how each type of account works and what it’s designed to do. Different savings account options support different needs, whether you're building an emergency fund, saving for a major purchase, or planning for retirement.

Share Savings Accounts

A share savings account is a foundational savings account that also establishes your membership with a credit union.

These accounts are designed to keep your money accessible while earning dividends over time. They’re simple to manage and work well for everyday savings, emergency funds, and shorter-term financial goals.

A share savings account is often a practical starting point for new savers or anyone who wants a straightforward place to build savings while maintaining easy access to funds.

Money Market Accounts

A money market account offers more flexibility than a traditional savings account while allowing you to earn more as your balance grows.

These accounts often include tiered dividend rates, meaning larger balances may earn higher dividends over time. Money market accounts are commonly used for larger emergency funds or savings goals that may take several years to reach.

A money market account is an excellent option if you want to maximize your earnings while keeping your savings accessible. Please note that a $2,500 minimum daily balance is required to waive the monthly service charge.

High-Yield Money Market Accounts

A high-yield money market account is designed for members with larger balances who want to earn more on their savings while still maintaining access to their funds.

Like standard money market accounts, these accounts may offer tiered dividend rates based on balance levels. However, they usually require a larger opening deposit or higher balance to qualify.

High-yield money market accounts are often used for larger financial goals, such as a home purchase, renovation project, or business expenses.

Special Savings Accounts

A special savings account is designed for a specific savings goal, such as:

- Vacations

- Holidays

- Weddings

- Vehicle purchases

- Other planned expenses

Having separate savings accounts for different goals can make it easier to stay organized and track your progress over time.

Special savings accounts allow you to deposit or withdraw funds as needed, and many people set up automatic transfers to build savings consistently. These accounts work well when you're saving for multiple short-term goals simultaneously.

Coverdell Education Savings Accounts

A Coverdell Education Savings Account is a tax-advantaged account designed to help families prepare for education expenses.

Funds can be used for qualified K-12 and college expenses, including:

- Tuition

- Books and supplies

- Fees

- Tutoring

- Computers

- Room and board

Contributions grow tax-free over time, and qualified withdrawals are also tax-free. Annual contribution limits apply.

A Coverdell Education Savings Account can be a useful option for families planning ahead for school-related costs.

Traditional IRA and SEP Accounts

Traditional IRAs and SEP IRAs are both designed to help individuals save for retirement.

Traditional IRAs are individual retirement accounts, while SEP IRAs are intended for self-employed individuals and small business owners. Both accounts use pre-tax contributions, and earnings grow tax-deferred until retirement withdrawals begin.

SEP IRAs generally allow much higher contribution limits than traditional IRAs.

These retirement accounts are often used by people focused on long-term retirement savings and tax advantages.*

Roth IRA Accounts

A Roth IRA is a retirement savings account funded with after-tax dollars. Because contributions are taxed before they are deposited, qualified withdrawals during retirement are tax-free.

Like traditional IRAs, Roth IRAs have annual contribution limits. Eligibility to contribute may also depend on your income level.

A Roth IRA may make sense if you expect to be in a higher tax bracket later on or want the benefit of tax-free retirement withdrawals.

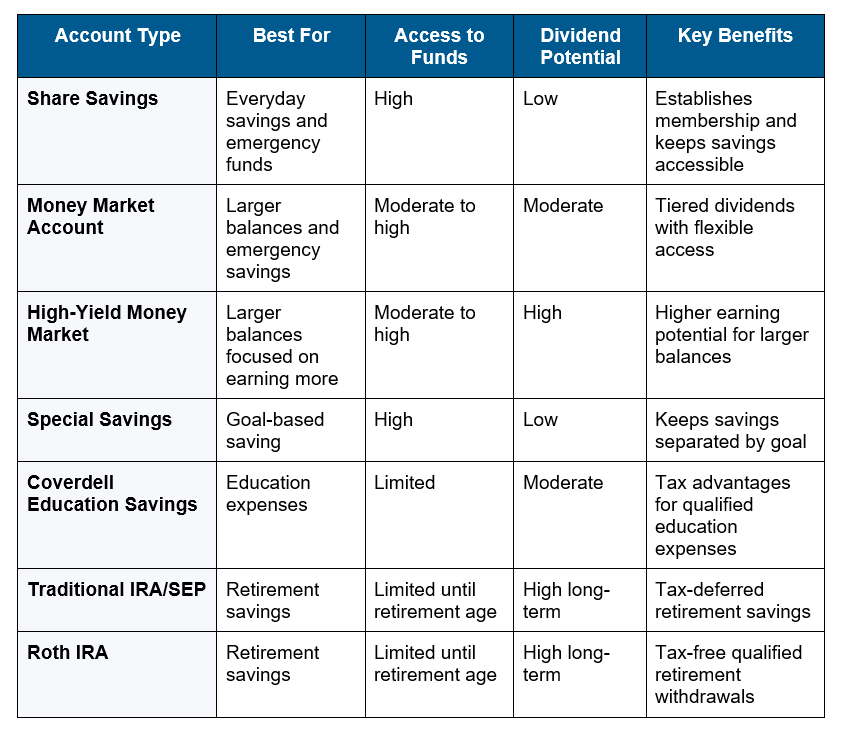

Savings Account Comparison

Seeing these savings accounts side by side can help you select the right option for your needs. Here's how they compare:

How to Choose a Savings Account

The right savings account depends on your financial goals and how you plan to use the money. These steps can help you narrow down your options.

1. Start with your savings goals

What are you saving for? Some accounts are better suited for everyday savings, while others are designed for education expenses or long-term retirement planning.

2. Consider when you’ll need access to the money

If you expect to use your funds soon, accessibility may matter more than earning potential. For longer-term goals, accounts with higher dividend potential may help your savings build over time.

3. Review account requirements

Before opening an account, compare:

- Minimum opening deposits

- Minimum balance requirements

- Withdrawal limitations

- Fees

- Contribution limits for retirement accounts

- Income eligibility requirements for retirement accounts

4. Consider using more than one account

Many people use separate accounts for different goals. For example, you might use a money market account for emergency savings, a special savings account for planned purchases, and a Roth IRA for retirement savings.

Find the Right Savings Accounts for Your Goals

There’s no one-size-fits-all approach to saving. The best savings account is the one that fits your financial goals, timeline, and how you plan to use your money.

Explore APGFCU’s savings account options to find an account that supports your savings goals today and in the future.

*Please consult your tax advisor.